Related

See More

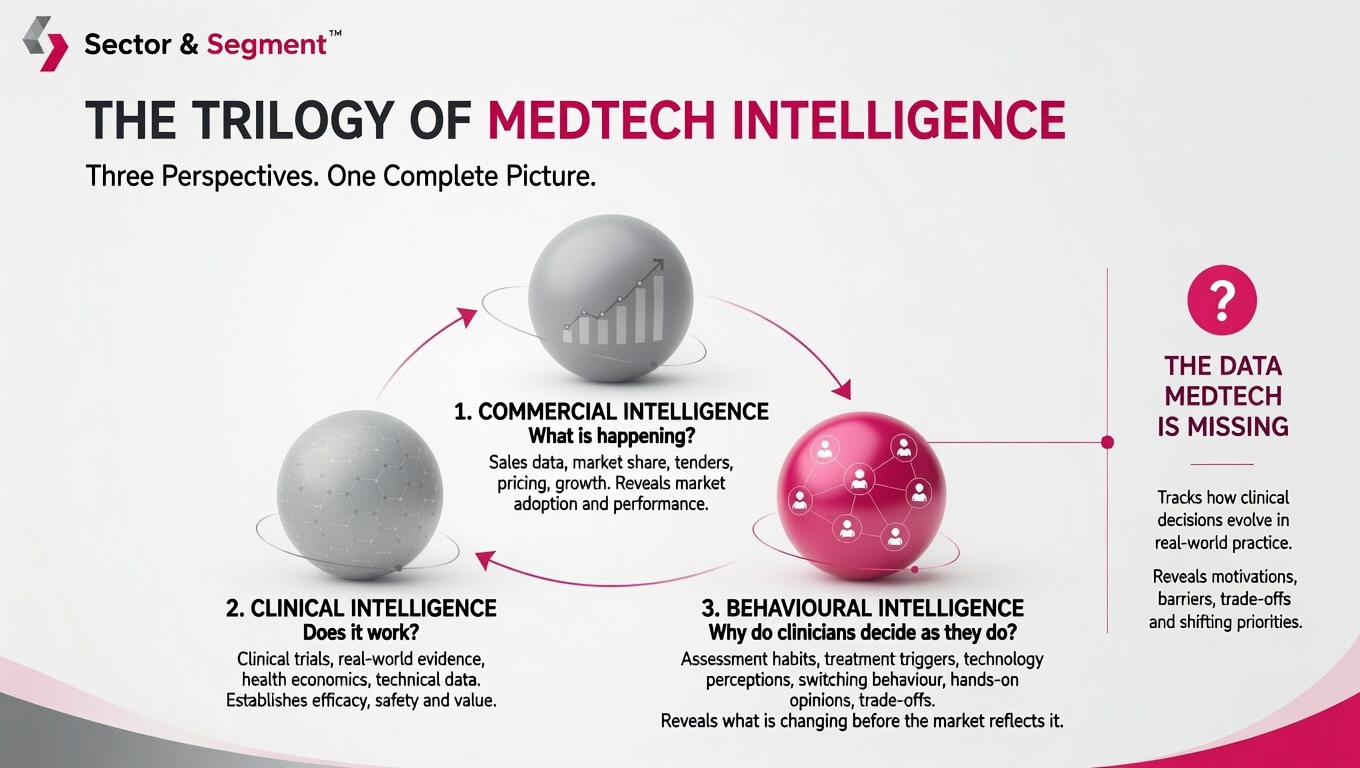

Cardiac implantable electronic devices, often referred to as CIEDs, have revolutionised the field of cardiology by providing life-saving interventions for patients with a variety of heart conditions. Due to increased prevalence of cardiovascular disease, driven primarily by an ageing population, the number of CIEDs implanted each year is expected to rise, with an estimated 1.4 million devices being implanted worldwide in 20171. Sector & Segment estimates Sector & Segment estimated the Global CIED market to be worth £22.3billion USD in 2023 and predicts it to grow to 35.3 billion by 2033.

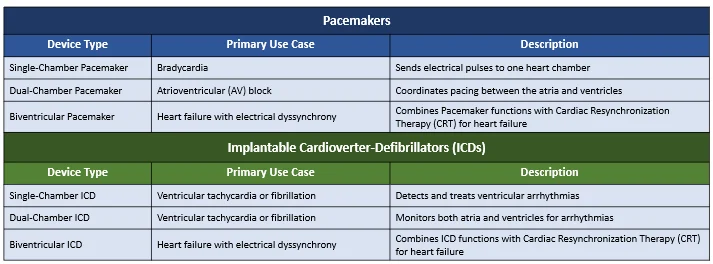

CIEDs come in many different forms, including pacemakers, implantable cardioverter-defibrillators (ICDs), and cardiac resynchronization therapy devices (CRTs), each tailored to address specific cardiac issues. Figure 1 displays a short summary of the options currently available.

While CIEDs have transformed the landscape of cardiac care, they are not without their challenges. Traditional CIEDs are comprised of a generator, containing the battery and electronic circuitry responsible for regulating the device, as well as two (three in the case of CRT) thin, insulated leads which carry electrical signals from the generator to the heart. It is these leads which have historically proven the “Achilles’ heel2” of CIEDs, as they are the most common cause of complications. In the rest of this article, we will delve deeper into the enduring concerns surrounding leads, the race towards a lead-free portfolio, the current roadblocks to widespread adoption, and how companies should navigate them.

As mentioned, lead-related complications are the most frequent type of complication CIED patients experience, regardless of CIED type. Kirkfeldt et. al analysed almost 6,000 Danish patients and found that within six months of implantation, 160 patients experienced a lead-related complication3. This accounted for just over 30% of all complications. In almost all cases, lead failures require either replacing the lead, or a full device revision, and can therefore have serious implications for patient health. Barreveld et. al assessed a registry of Dutch patients implanted with an ICD and calculated a mean cost of lead-related complications of €5,800, higher than most other common complications4.

There are a large variety of reasons leads can fail, which can broadly be categorised into:

Further, issues related to the ‘pocket’ created outside the heart where the generator has to be placed, such as infections and hematomas, as well as pulse generator issues, are also common causes of complications in devices involving leads.