Related

See More

In recent years, the intricate connection between gastrointestinal and mental well-being has emerged as a promising avenue for scientific exploration. Termed the gut-brain axis, the complex communication network between the gut microbiota and the central nervous system has revealed a new frontier in understanding the interplay between one’s gastrointestinal wellbeing and multiple facets of brain function, most notably mental health and cognitive performance. As our understanding of the link between the gut and the brain deepens, the theoretical case for utilizing probiotics to enhance both mental health and cognitive performance grows stronger. Although the evidence for consuming probiotics for mental well-being is still in its infancy, this class of probiotics, commonly referred to as psychobiotics, has firmly captured the attention of both academia and industry. As psychobiotics become an increasingly popular topic of discussion in mainstream media, consumer demand has also rapidly begun to grow. Amazon sales data from ClearCut Analytics1 showed that whilst the American probiotic market as a whole grew by 18% in 2022, sales of probiotic products marketed for mood support grew by 33%.

In this paper, we delve into some of the key factors driving this consumer demand, and consequently why psychobiotics are a promising investment opportunity for VMHS companies in both the present and future. We provide a quick overview of the current regulatory landscape in some of the largest markets, which depicts a cautiously optimistic outlook for the future. We conclude with some strategic considerations for how manufacturers should position their psychobiotics.

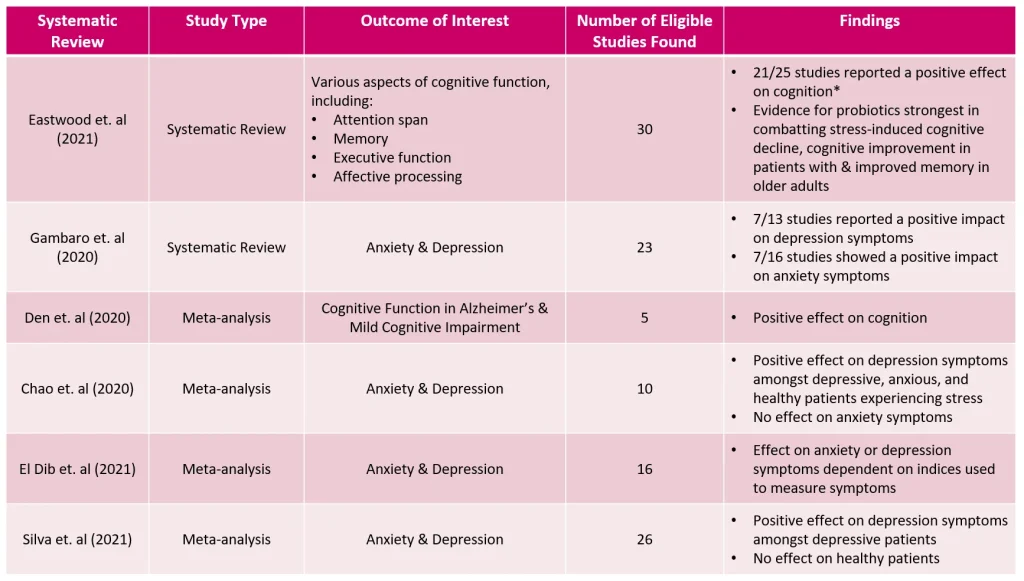

The benefits of consuming probiotics for “gut health”, i.e., helping to prevent and/or alleviate gastrointestinal symptoms and/or illnesses, have been well established2. What is less well established is how, through the gut-brain axis, many of the same probiotic strains can have positive influences on both an individual’s cognitive performance and mental health. This research is still very much in its infancy. A decade ago, much of the evidence supporting this connection came from animal studies, with limited research conducted in humans. In recent years, however, there has been a notable shift towards human studies, demonstrating progress towards establishing proven psychobiotic effects in individuals. Table 1 summarises some of the most prominent literature reviews restricted to humans only.

Eastwood et. al (2021)3 conducted a systematic review on the effect of administering probiotics on cognition and reported a positive effect in 21/25 studies. Den et. al (2020)4focused their meta-analysis on patients with Alzheimer’s and mild cognitive impairment and found that cognitive performance was greatly improved in both groups. Gambaro et. al (2020)5 focused their review instead on the effect on anxiety and depression, demonstrating that probiotics improved depression and anxiety symptoms in 53.83% and 43.75% studies, respectively. Chao. et al (2020)6 conducted a meta-analysis of RCTs comparing patients with anxiety or depression against healthy patients. They found probiotics to reduce depression scores for patients with anxiety and/or depression, as well as healthy patients under stress. However, they found no reduction in anxiety symptoms amongst any of these groups. Similarly, El Dib et. al (2021)7 found probiotics to improve depression and anxiety symptoms only when certain depression and anxiety indices were used. Finally, Silva et. al (2021)8 found probiotics to have a significant effect on depressive symptoms in patients already diagnosed with depression, but not in healthy patients.

*5 studies on young children were excluded due to confounding factors, particularly neurocognitive development being too rapid at this age to see any effect of probiotic intervention

The evidence to date remains mixed, with most reviews concluding that more large scale RCTs are required. And the lack of available RCTs means strain-specific reviews are, to date, unavailable. That being said, most reviews to date conclude on an optimistic note regarding the potential of strains developed specifically for mental wellbeing. The large number of studies demonstrating at least a modest cognitive benefit, combined with the low cost and risk profiles of probiotics, make it a very appealing area to watch for academics, healthcare professionals, and consumers alike.

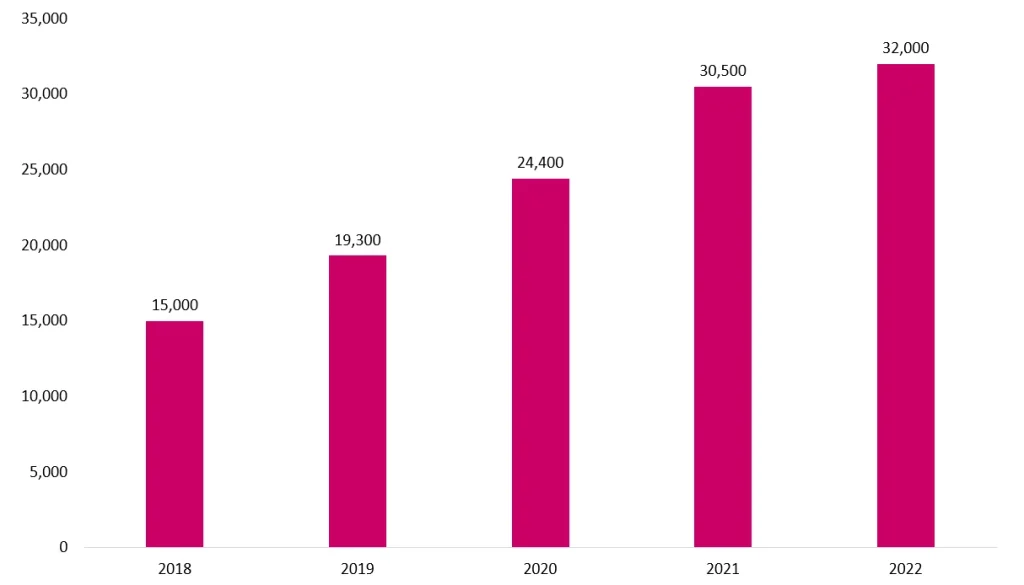

Although more evidence will be needed to achieve widespread acceptance in the eyes of both academia and regulators, increased demand for psychobiotics is likely also being driven by the rapidly growing body of evidence of the gut-brain axis in general. Between 2018 and 2022, the number of papers published referencing the gut-brain axis more than doubled from 15,000 to 32,000 (see below).

Meanwhile, a 2021 survey by the IFIC (International Food Information Council)9 found that the most common reason cited for consuming probiotics was to support gut health (51%), ahead of general health and wellness (38%). Since probiotics are considered almost synonymous with the gut, an increased understanding of the gut-brain axis will likely drive probiotic demand without all consumers demanding causal evidence. Despite the relative novelty of the gut-brain axis in contemporary discourse, the same survey showed that 13% of probiotics consumers already claim to take probiotics for their mood and emotional health.

Demand for psychobiotics is also likely being driven by rapidly increasing prevalence rates of mental health disorders. A 2022 study by Healthy Marketing Team found that mental wellbeing has become the top health trend expected to drive consumer supplement choices10. The World Health Organisation estimates that approximately 280 million people in the world have depression, a comparable number of people have anxiety, and that both these figures increased by roughly 25% during the COVID-19 pandemic11.

Increased emphasis, awareness and destigmatisation around seeking treatment for mental health issues, particularly in high-income and western markets, may also be driving demand. A 2019 survey by Alight showed that 2,500 US office workers ranked mental health as the second most important aspect of their wellbeing, ahead of physical and social (the number one aspect was financial)12.

Conversely, mental health still carries a significant stigma in many societies. The simplicity, discretion, and relative affordability of integrating psychobiotics into one’s lifestyle may appeal to those who have been hesitant to explore traditional mental health treatments.

The broader wellness and self-care movements have also heavily contributed to the increase in psychobiotic demand. A 2021 survey by McKinsey of 7500 consumers located in the US, UK, China, Japan, Brazil, and Germany showed an increase in the prioritisation of wellness across all six markets13. 42% of respondents considered wellness to be a top priority, and respondents unanimously defined wellness as encompassing both physical and mental health.

Consumers are now more proactive in taking charge of their health and well-being than ever, seeking out products that offer preventive benefits beyond merely addressing symptoms. Additionally, these consumers have shown increased demand for products which they deem ‘natural’, as well as products which can offer multiple health benefits at once. Psychobiotics align perfectly with this trend, offering a proactive and preventive strategy for maintaining both mental and gastrointestinal wellbeing. As psychobiotics are widely available in multiple forms, including supplements, fortified foods, and functional beverages, the ease of incorporating them into one’s daily routine, as well as finding the psychobiotics best suited to one’s own body, is very appealing to those consumers who value wellness.

As previously mentioned, sales of probiotics marketed for mood grew at 33% on Amazon in the US in 2022, making it the fastest growing segment of the probiotic market. Despite this sharp increase in demand, the market for psychobiotics has a long way to go to catch up to probiotics marketed for gut health. Sales for probiotics with a pure digestive health focus actually experienced a slight decline (-0.2%) in 2022, but remained the largest segment at $130 million, compared to a mere $4.4m for mood-focused probiotics.

We focused our analysis on the US supplement market as it has a uniquely high use of supplements, with 30% of consumers choosing to get their probiotics from supplements rather than natural foods like yogurt (the next closest market was the EU at 14%)14. Amazon.com provides a good lens through which to analyse the US supplement market, as a survey by Trust Transparency showed that 55% of US consumers purchased their supplements online15 and Amazon naturally accounts for the lion’s share of those sales. Online supplement sales have also been the fastest growing sector for supplement sales throughout the last decade, which was further accelerated due to the COVID-19 pandemic.

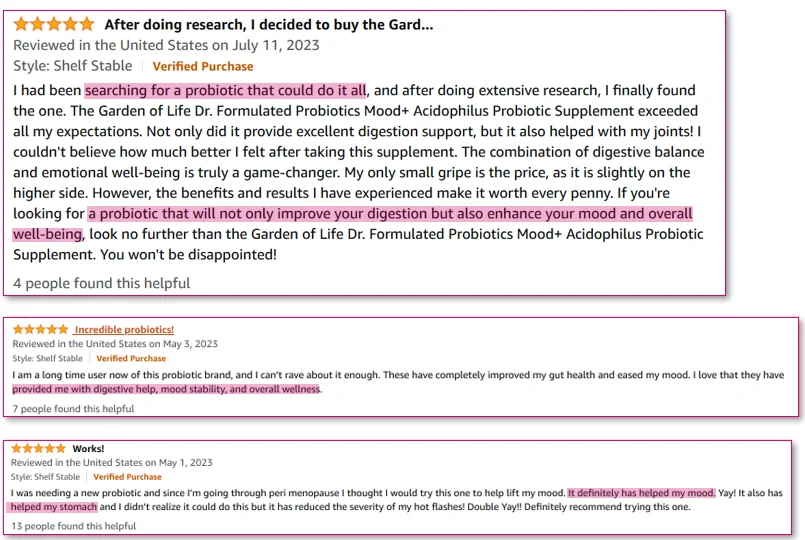

A quick analysis of the Amazon marketplace for psychobiotics shows that it is particularly fragmented. Research by Clavis Insights16 shows that the minimum number of reviews needed for a product on Amazon to be competitive is 21. Of the hundreds of psychobiotics available on Amazon which meet this minimum criterion, the average number of reviews is well below 100. Only three products received over 1,000 reviews, of which the clear market leader is Garden of Life’s “Mood+” with 6000 reviews and over 10,000 bottles sold per month. Figure 2 showcases the current top three highest selling psychobiotics on Amazon, contrasted with four of the most popular probiotics positioned for gut health.

Such fragmentation may demonstrate a lack of consumer loyalty (a survey by Accelerate Associates showed that 75% of consumers would be willing to switch supplement brands17), but the lack of a dominant company or product can also be interpreted as a signal that the market has yet to be ‘won’. The barrier to entry for psychobiotics will be comparatively lower than other probiotic market segments with strong incumbents, and the lack of consumer loyalty means that anyone can currently compete. Finally, fragmented markets offer a greater opportunity for product differentiation. Manufacturers have the ability to tailor their products to specific mental health concerns and carve out a distinct market presence.

One of the more surprising findings is that, despite the comparative lack of evidence for probiotics and mental wellbeing, consumer reviews are largely comparable to the average of probiotics across categories. An examination of consumer reviews by Lumina Intelligence between 2017 and 2020 across 1400+ brands and 25 markets showed an average review of 4.47 stars out of 5 for probiotics positioned for mental wellbeing, as opposed to 4.53 across all probiotics18.

Analysing the consumer reviews of the top three products on Amazon.com highlights how probiotics align well with the aforementioned trends of holistic health, products with multifaceted benefits, and general wellness, which in turn results in consumer satisfaction.